A neat little tool that shows what students pay for college per school, as well as other interesting information. |

|

Debt CounterA debt counter for the current total amount of student loan debt in the United States.

|

What is a Private Loan? What is a Federal Loan?

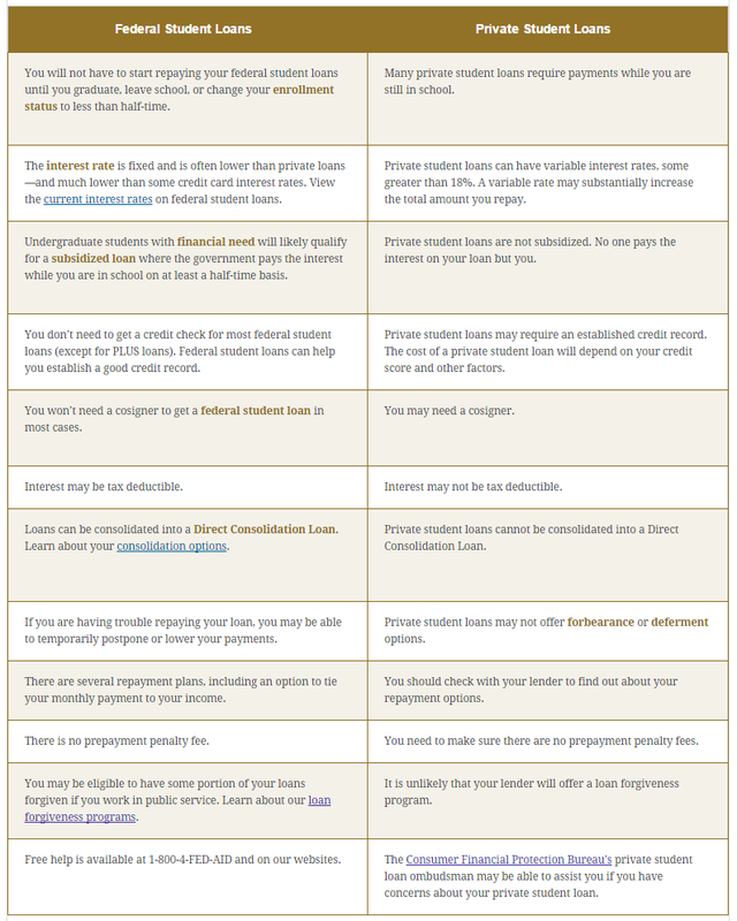

Federal/Direct - A federal loan, sometimes called a "direct loan", is a loan that is supplied to a lender by the government, which is then provided to a student. A Defense to Repayment would affect federal loans when submitted and when approved.

Private - Private loans are non-federal loans, made by a lender such as a bank, credit union, state agency, or a school. A Defense to Repayment does not apply to private loans.

More information on the differences between these types of loans can be found below.

Private - Private loans are non-federal loans, made by a lender such as a bank, credit union, state agency, or a school. A Defense to Repayment does not apply to private loans.

More information on the differences between these types of loans can be found below.

What happens if you don't pay your loans?

If you don't pay your private loans to companies like Navient, AES, or Great Lakes for example, then the following will occur initially:

If you don't pay your federal loans, then the government will begin doing similar to what was mentioned above, sometimes without notification:

- Collection Tactics (1) - You will be harassed with phone calls and letters in the mail. Some tactics are illegal though. Learn what collectors can and cannot do by visiting this link to help protect yourself and know your rights.

- Collection Tactics (2) - Your friends and family members will also probably be harassed. This is illegal, so don't let it happen. More information here.

- Collection Tactics (3) - Your employer might be contacted. Again, this is not legal. The employer can request that they stop calling, and they must then abide by their request. More info is again here.

- Assignment to a Collection Agency - After a certain period of time, your account will be handed over to a collection agency. You will have to deal with that collection agency until your account is brought up-to-date. They will use similar tactics as your original loan company to contact you and try and get you to pay on the debt. (*Note - Be sure to ask the collection agency if they can verify the debt you owe. Sometimes during this transition from loan company to collection agency, documents can be lost or the loan company just doesn't provide those documents to the collection agency. Without proof of your debt, they will have a difficult time in collecting from you.)

- Possible Lawsuit - Finally, if the collection agency fails to get you to pay on your private loans, then the loan company will probably take you to court. This can be expensive for the loan company, so they probably do not want to go this route. If they do, then they will attempt to have a judge rule in their favor to garnish your wages, social security, and tax returns. This will only happen if a judge rules against you though. If you stayed in contact with the lender and tried to work with them but they didn't help you out (allow smaller payments, lower interest, etc.), then that will help your case.

If you don't pay your federal loans, then the government will begin doing similar to what was mentioned above, sometimes without notification:

- Wage Garnishment - Your lender may garnish up to 15% of your disposable income. Payments recovered through wage garnishment are not considered voluntary and would not stop additional collection activity or qualify a loan for Rehabilitation.

- Federal Treasury Offset - In addition to wage garnishment, your lender may advise the Federal Treasury of your unpaid debt which will be deducted from your eligible federal tax refunds or your income, commonly referred to as an "offset."

- Assignment of the debt to the United States Department of Education (USDE) - If your lender determines that your debt is uncollectable, they might permanently assign the debt to the USDE for additional federal collection action.

Loan Discharge Eligibility (Federal Loans)

If your school closed while you were attending, you may be eligible for a discharge* of your federal loans under the Closed School Discharge Program, which includes any payments you made voluntarily or through collections. You qualify for a full loan discharge if you meet the following requirements:

You are ineligible if you:

- If the school closed while you were enrolled and you don't complete your program because of the closure

- If the school closed within 120 days after you withdraw

You are ineligible if you:

- Withdraw from the school 120 days or more before the school closes

- You are completing a comparable education program at another school, such as a "partner school" with Westwood College (non-comparable education programs may qualify you for a loan discharge)

- You've agreed to participate in a "teach out" with the school

- If you transfer academic credits/hours earned from Westwood to another school

- If you've completed all coursework for your specific program, even if you haven't received a diploma/certificate from the school

Loan Discharge Eligibility (Private Loans)

If your school closed while you were attending, you may be eligible for a discharge* of your private loans. This might be more difficult to achieve since you'll have to deal with the private student loan lender directly. Some states do offer a little assistance though. For example, under the Student Tuition Recovery Fund in California, you may qualify for loan discharge if you meet the following requirements:

Other states that DO provide assistance with discharging of your private loans include:

States that do NOT provide assistance like the Student Tuition Recovery Fund at the time of this writing (02/23/2016) include:

- If you prepaid your tuition

- If you paid the Student Tuition Recovery Fund fee (probably included with your prepayment, if you made one)

- If you suffered a loss (i.e., lost an education, will lose money on loans for a school that is no longer in business, etc.)

Other states that DO provide assistance with discharging of your private loans include:

- Georgia - Tuition Guarantee Trust Fund (770) 414-3300

- Virginia - Student Tuition Guarantee Fund (804) 225-2600

States that do NOT provide assistance like the Student Tuition Recovery Fund at the time of this writing (02/23/2016) include:

- Colorado

- Illinois

PLEASE BE AWARE - In order to get out of refunding any loans, a school will offer you a "teach out" to cover themselves. A "teach out" benefits a school in two ways:

- This allows the school to create an arbitrary closing date. This makes it extremely difficult for a student to withdraw from the school and meet the 120 day requirements mentioned above.

- The school has each student participating in a "teach out" sign documentation that relinquishes their rights for a refund.

Additional information - Know the difference between a Private Loan and a Federal/Direct Loan

Student loans (Federal/Direct) - A federal loan, sometimes called a "direct loan", is a loan that is supplied to a lender by the government, which is then provided to a student. These type of loans usually have lower interest rates and more flexible repayment options, though this is not always the case. Student loan options can be overwhelming at first glance. But when it comes to federal student loans, there are just a few options.

|

Subsidized Stafford Loan

The subsidized Stafford Loan is available to students who qualify for need as determined by the FAFSA. Students must be a U.S. citizen or eligible non-citizen as well as have a high school diploma or GED. Like most federal student loans, interest does not accrue while the student is in school. If students qualify for a subsidized Stafford Loan, it will be stated on their award letter notification along with the amount for which they can borrow. Again, a Subsidized loan is a loan for students with demonstrated financial need, as determined by federal regulations. No interest is charged while a student is in school at least half-time, during the grace period, and during deferment periods. Perkins Loan The Perkins Loan is another federal loan option that is for needy students. Students must be a U.S. citizen or eligible non-citizen as well as hold a high school diploma or GED. Again, interest does not accrue with the Perkins Loan, and students will find out whether or not they qualify as well as for how much when they receive their award letters from colleges. A Perkins loan is available to undergraduate, graduate, and professional students with exceptional financial need. The current interest rate for this loan is 5%. Not all schools participate in the Federal Perkins Loan Program. You should check with your school's financial aid office to see if your school participates. Your school is the lender; you will make your payments to the school that made your loan or your school’s loan servicer. Funds depend on your financial need and the availability of funds at your college. Unsubsidized Stafford Loan The unsubsidized Stafford Loan is a little different from other federal loans. For both the subsidized Stafford and Perkins Loans, students must qualify for need as determined by the FAFSA. However, the unsubsidized Stafford Loan is available to any student, regardless of need. Also, unlike the other federal loans, interest accrues while the student is attending school. Again, the unsubsidized Stafford Loan is not based on financial need; interest is charged during all periods, even during the time a student is in school and during grace and deferment periods. PLUS Loan A PLUS Loan is an unsubsidized loan for the parents of dependent students and for graduate/professional students. PLUS loans help pay for education expenses up to the cost of attendance minus all other financial assistance. Interest is charged during all periods. PLUS loan borrowers cannot have an adverse credit history (a credit check will be done). If you are determined to have an adverse credit history, you may still receive a Direct PLUS Loan if you obtain an endorser who does not have an adverse credit history. An endorser is someone who agrees to repay the Direct PLUS Loan if you do not repay the loan. If you are a parent borrowing on behalf of your dependent student, the endorser may not be the student on whose behalf you (the parent) obtain a Direct PLUS Loan. In some cases, you may also be able to obtain a Direct PLUS Loan if you document to our satisfaction that there are extenuating circumstances related to your adverse credit history. (Source) (Source 2) (Source 3) (Source 4) |

Student loans (Private) - Private loans are non-federal loans, made by a lender such as a bank, credit union, state agency, or a school. Private student loans can have variable interest rates, some greater than 18%. A variable rate may substantially increase the total amount you repay. Private student loans are not subsidized. No one pays the interest on your loan but you. It is also unlikely that your lender will offer a loan forgiveness program. (Source)

Student Loan Consolidation

Consolidation Loans combine several student or parent loans into one bigger loan from a single lender, which is then used to pay off the balances on the other loans. They also provide an opportunity for alternative repayment plans, making monthly payments more manageable. The downsides to consolidating are:

- 1.) The amount of time you pay on the loan increases when you consolidate.

- 2.) Interest rates on consolidation loans are locked in at a fixed rate and will not change.

Consolidation loans are available for most federal loans, including Stafford, PLUS and SLS, FISL, Perkins, Health Professional Student Loans, NSL, HEAL, Guaranteed Student Loans and Direct loans. Some lenders offer private consolidation loans for private education loans as well.

(*Reminder - if you consolidate your loans, you will likely be restarting the life of your loan terms from the beginning. This means that if you paid 3 years on a 10 year loan, you would have only 7 years left. BUT, if you consolidate the loans you've been paying on, that 10-year term will reset and you'll have to pay your loans for 10 years again, essentially making you pay your loans for 13 years instead of 10. Be sure to ask about what would happen to your loan term if you were to consolidate before actually going through with it so that you can make the proper decision.)

Interest Rates

The interest rate on a consolidation loan is the weighted average of the interest rates on the loans being consolidated, rounded up to the nearest 1/8 of a percent. That interest rate is fixed for life.

For example, suppose a student has just unsubsidized Stafford Loans originated on or after July 1, 2006. These loans have a fixed interest rate of 6.8%. When they are consolidated by themselves, the consolidation loan will have an interest rate of 6 and 7/8ths of a percent, or 6.875%. So the interest rate increases only slightly.

If the borrower has a mix of loans with different interest rates, the weighted average will be somewhere in between. For example, if the borrower has $5,000 of Perkins Loans (at 5.0%) and $10,000 of unsubsidized Stafford Loans (at 3.86%), the weighted average is

$5,000 * 5.0% + $10,000 * 3.86% ------------------------------ = 4.24% $5,000 + $10,000

This weighted average, 4.2%, is then rounded up to the nearest 1/8th of a percent, yielding a consolidation loan interest rate of 4.25%.If you are consolidating loans with different interest rates, the weighted average interest rate will always be in between. Don't be fooled if someone tries to suggest that this will save you money by getting you a lower interest rate. The interest rate may be lower than the highest of your interest rates, but it is also higher than the lowest of your interest rates. More importantly, the amount of interest you pay over the lifetime of the loan will be about the same.

No Cost to Consolidate

Aside from a slight increase in the interest rate on the consolidation loan, there is no cost to consolidate your loans. There are no fees to consolidate.

Under no circumstances pay a fee in advance to get a federal education loan or consolidate your federal education loans. There are no fees to consolidate your loans. While other federal education loans, such as the Stafford and PLUS loans, may charge some fees, the fees are always deducted from the disbursement check. There is never an upfront fee. If someone wants you to pay an upfront fee, chances are that it is an example of an advance fee loan scam.

Who Can Consolidate

Both student and parent borrowers can consolidate their education loans. Students and parents cannot combine their loans through consolidation, since only loans from the same borrower can be consolidated. But they can consolidate their loans separately.

Students can consolidate their education loans only during the grace period or after the loans enter repayment. Loans that are in default but with satisfactory repayment arrangements may also be consolidated. Students can no longer consolidate while they are still in school. Parents, however, can consolidate PLUS loans at any time.

Which Loans Can be Consolidated?

Any federal education loan can be consolidated. You can even consolidate a single loan. There are, however, a few restrictions on consolidating a consolidation loan.

You can consolidate a consolidation loan only once. In order to re-consolidate an existing consolidation loan, you must add loans that were not previously consolidated to the consolidation loan. You can also consolidate two consolidation loans together. But you cannot consolidate a single consolidation loan by itself.

Note that when you reconsolidate a consolidation loan, it does not relock the rates on the consolidation loan. The consolidation loan is treated as a fixed rate loan within the weighted average interest rate formula used to calculate the interest rate on the new consolidation loan.

Repayment Plans

Consolidation loans provide access to several alternate repayment plans besides standard ten-year repayment. These include extended repayment, graduated repayment, income contingent repayment (Direct Loans only) and income sensitive repayment (FFEL only). If you do not specify the repayment terms, you will receive standard ten-year repayment.

Consolidation loans often reduce the size of the monthly payment by extending the term of the loan beyond the 10-year repayment plan that is standard with federal loans. Depending on the loan amount, the term of the loan can be extended from 12 to 30 years. The reduced monthly payment may make the loan easier to repay for some borrowers. However, by extending the term of a loan the total amount of interest paid over the lifetime of the loan is increased.

You do not need to pick an alternate repayment plan. We recommend sticking with standard ten-year repayment, because it will save you money. The alternate repayment plans may have lower monthly payments, but this increases the term of the loan and the total interest paid over the lifetime of the loan.

Repayment on a consolidation loan will begin within 60 days of disbursement of the loan, unless the borrower qualifies for a deferment or forbearance.

(Source)

(*Reminder - if you consolidate your loans, you will likely be restarting the life of your loan terms from the beginning. This means that if you paid 3 years on a 10 year loan, you would have only 7 years left. BUT, if you consolidate the loans you've been paying on, that 10-year term will reset and you'll have to pay your loans for 10 years again, essentially making you pay your loans for 13 years instead of 10. Be sure to ask about what would happen to your loan term if you were to consolidate before actually going through with it so that you can make the proper decision.)

Interest Rates

The interest rate on a consolidation loan is the weighted average of the interest rates on the loans being consolidated, rounded up to the nearest 1/8 of a percent. That interest rate is fixed for life.

For example, suppose a student has just unsubsidized Stafford Loans originated on or after July 1, 2006. These loans have a fixed interest rate of 6.8%. When they are consolidated by themselves, the consolidation loan will have an interest rate of 6 and 7/8ths of a percent, or 6.875%. So the interest rate increases only slightly.

If the borrower has a mix of loans with different interest rates, the weighted average will be somewhere in between. For example, if the borrower has $5,000 of Perkins Loans (at 5.0%) and $10,000 of unsubsidized Stafford Loans (at 3.86%), the weighted average is

$5,000 * 5.0% + $10,000 * 3.86% ------------------------------ = 4.24% $5,000 + $10,000

This weighted average, 4.2%, is then rounded up to the nearest 1/8th of a percent, yielding a consolidation loan interest rate of 4.25%.If you are consolidating loans with different interest rates, the weighted average interest rate will always be in between. Don't be fooled if someone tries to suggest that this will save you money by getting you a lower interest rate. The interest rate may be lower than the highest of your interest rates, but it is also higher than the lowest of your interest rates. More importantly, the amount of interest you pay over the lifetime of the loan will be about the same.

No Cost to Consolidate

Aside from a slight increase in the interest rate on the consolidation loan, there is no cost to consolidate your loans. There are no fees to consolidate.

Under no circumstances pay a fee in advance to get a federal education loan or consolidate your federal education loans. There are no fees to consolidate your loans. While other federal education loans, such as the Stafford and PLUS loans, may charge some fees, the fees are always deducted from the disbursement check. There is never an upfront fee. If someone wants you to pay an upfront fee, chances are that it is an example of an advance fee loan scam.

Who Can Consolidate

Both student and parent borrowers can consolidate their education loans. Students and parents cannot combine their loans through consolidation, since only loans from the same borrower can be consolidated. But they can consolidate their loans separately.

Students can consolidate their education loans only during the grace period or after the loans enter repayment. Loans that are in default but with satisfactory repayment arrangements may also be consolidated. Students can no longer consolidate while they are still in school. Parents, however, can consolidate PLUS loans at any time.

Which Loans Can be Consolidated?

Any federal education loan can be consolidated. You can even consolidate a single loan. There are, however, a few restrictions on consolidating a consolidation loan.

You can consolidate a consolidation loan only once. In order to re-consolidate an existing consolidation loan, you must add loans that were not previously consolidated to the consolidation loan. You can also consolidate two consolidation loans together. But you cannot consolidate a single consolidation loan by itself.

Note that when you reconsolidate a consolidation loan, it does not relock the rates on the consolidation loan. The consolidation loan is treated as a fixed rate loan within the weighted average interest rate formula used to calculate the interest rate on the new consolidation loan.

Repayment Plans

Consolidation loans provide access to several alternate repayment plans besides standard ten-year repayment. These include extended repayment, graduated repayment, income contingent repayment (Direct Loans only) and income sensitive repayment (FFEL only). If you do not specify the repayment terms, you will receive standard ten-year repayment.

Consolidation loans often reduce the size of the monthly payment by extending the term of the loan beyond the 10-year repayment plan that is standard with federal loans. Depending on the loan amount, the term of the loan can be extended from 12 to 30 years. The reduced monthly payment may make the loan easier to repay for some borrowers. However, by extending the term of a loan the total amount of interest paid over the lifetime of the loan is increased.

You do not need to pick an alternate repayment plan. We recommend sticking with standard ten-year repayment, because it will save you money. The alternate repayment plans may have lower monthly payments, but this increases the term of the loan and the total interest paid over the lifetime of the loan.

Repayment on a consolidation loan will begin within 60 days of disbursement of the loan, unless the borrower qualifies for a deferment or forbearance.

(Source)

Private Student Loan Consolidation

(*Note that if you consolidate your loans, you will likely be restarting the life of your loan terms from the beginning. This means that if you paid 3 years on a 10 year loan, you would have only 7 years left. BUT, if you consolidate the loans you've been paying on, that 10-year term will reset and you'll have to pay your loans for 10 years again, essentially making you pay your loans for 13 years instead of 10. This will also increase the overall cost of your loans, since more time means more interest can accrue. Be sure to ask about what would happen to your loan term if you were to consolidate before actually going through with it so that you can make the proper decision.)

Private student loans cannot, in general, be consolidated with federal student loans. The low interest rates on federal consolidation loans are not available to private education loans. Nevertheless, there are several options for refinancing private education loans.

Since most private education loans do not compete on price, a private consolidation loan is merely replacing one or more private education loans with another. So the main benefit of such a consolidation is obtaining a single monthly payment. Also, since the consolidation resets the term of the loan, this may reduce the monthly payment (at a cost, of course, of increasing the total interest paid over the lifetime of the loan).

However, since the interest rates on private student loans are based on your credit score, you may be able to get a lower interest rate through a private consolidation loan if your credit score has improved significantly since you first obtained the loan. For example, if you've graduated and now have a good job and have been building a good credit history, your credit score may have improved. If your credit score has increased by 50-100 points or more, you may be able to get a lower interest rate by consolidating your debt with another lender. You can also try talking to the current holder of your loans, to see if they'll reduce the interest rate on your loans rather than lose your loans to another lender.

Home Equity Loans

Private education loans tend to have interest rates that are in the same ballpark as home equity loans. If your private education loan has a variable interest rate, you might consider using a fixed rate home equity loan to pay off the private education loan, effectively locking in the interest rate.

Education Lenders

The following education lenders will consolidate private education loans. These are private consolidation programs, so the interest rates are dictated by the lender, not the government. There may be additional fees charged for originating these loans.

You should not consolidate your federal student loans together with your private education loans. They should be consolidated separately, as the federal consolidation loans offer superior benefits and lower interest rates for consolidating federal student loans.

When evaluating a private consolidation loan, ask whether the interest rate is fixed or variable, whether there are any fees, and whether there are prepayment penalties.

For the most updated information, it’s best to check the individual lender websites.

(Source)

Private student loans cannot, in general, be consolidated with federal student loans. The low interest rates on federal consolidation loans are not available to private education loans. Nevertheless, there are several options for refinancing private education loans.

Since most private education loans do not compete on price, a private consolidation loan is merely replacing one or more private education loans with another. So the main benefit of such a consolidation is obtaining a single monthly payment. Also, since the consolidation resets the term of the loan, this may reduce the monthly payment (at a cost, of course, of increasing the total interest paid over the lifetime of the loan).

However, since the interest rates on private student loans are based on your credit score, you may be able to get a lower interest rate through a private consolidation loan if your credit score has improved significantly since you first obtained the loan. For example, if you've graduated and now have a good job and have been building a good credit history, your credit score may have improved. If your credit score has increased by 50-100 points or more, you may be able to get a lower interest rate by consolidating your debt with another lender. You can also try talking to the current holder of your loans, to see if they'll reduce the interest rate on your loans rather than lose your loans to another lender.

Home Equity Loans

Private education loans tend to have interest rates that are in the same ballpark as home equity loans. If your private education loan has a variable interest rate, you might consider using a fixed rate home equity loan to pay off the private education loan, effectively locking in the interest rate.

Education Lenders

The following education lenders will consolidate private education loans. These are private consolidation programs, so the interest rates are dictated by the lender, not the government. There may be additional fees charged for originating these loans.

You should not consolidate your federal student loans together with your private education loans. They should be consolidated separately, as the federal consolidation loans offer superior benefits and lower interest rates for consolidating federal student loans.

When evaluating a private consolidation loan, ask whether the interest rate is fixed or variable, whether there are any fees, and whether there are prepayment penalties.

For the most updated information, it’s best to check the individual lender websites.

(Source)

More information to come on the following topics...

- Know who your lenders are.

- Know how many loans you have.

- Know the total for each of your loans.

- Know the interest rate on each of your loans, as well as what types of interest rate (Fixed vs Variable).

- Know the life of each of your loans.

- Know when your first payment is due, and whether you need to pay while in school or not.

- Know how much of your monthly payments are going to interest, and how much is actually paying down your overall loan(s).

- Know which of your loans have cosigners (if any), and which do not.

- Find out if your lender gives the option to request to release your co-signer from the loans in which they co-signed for.

- Why have my loans been handed off to a new lender?

- Know how many loans you have.

- Know the total for each of your loans.

- Know the interest rate on each of your loans, as well as what types of interest rate (Fixed vs Variable).

- Know the life of each of your loans.

- Know when your first payment is due, and whether you need to pay while in school or not.

- Know how much of your monthly payments are going to interest, and how much is actually paying down your overall loan(s).

- Know which of your loans have cosigners (if any), and which do not.

- Find out if your lender gives the option to request to release your co-signer from the loans in which they co-signed for.

- Why have my loans been handed off to a new lender?

- Know the difference between Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), and Pay As You Earn Repayment (PAYER) Link

- Know what type of payment is right for you. This includes your current payment plan, the three repayment plans mentioned above, or whether you should consolidate.

- Know what Defense To Repayment is and how to apply. You will also need to know the laws in your state that relate to this.

- Know the Bankruptcy options for you, and what the consequences might be if you successfully claim bankruptcy.

- Know which government jobs help pay off your loans.

- Know what type of payment is right for you. This includes your current payment plan, the three repayment plans mentioned above, or whether you should consolidate.

- Know what Defense To Repayment is and how to apply. You will also need to know the laws in your state that relate to this.

- Know the Bankruptcy options for you, and what the consequences might be if you successfully claim bankruptcy.

- Know which government jobs help pay off your loans.

| title_iv_loan_eligibilty.pdf |